If you have started exploring what your CPA firm or accounting practice is worth, you have likely run into two different earnings metrics in the same conversation: EBITDA and SDE. They sound similar. They are not the same. And the one a buyer applies to your firm can change the final selling price by hundreds of thousands of dollars.

We have spent more than 15 years valuing and selling accounting practices less than $5 million in revenue, and we see this confusion regularly, especially now that private equity and roll-up buyers have entered the CPA acquisition space. Here is a plain-English breakdown of what each metric means, when each one applies, and why it matters in your sale.

What is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is the standard cash flow metric used by larger companies, institutional investors, and private equity firms. EBITDA assumes the company is run by professional management who are paid a market-rate salary, and the metric measures the operating earnings the business produces independent of the owner’s personal compensation.

EBITDA is the dominant metric in the lower-middle market and above M&A space, including most private equity (PE) transactions. Private equity is buying CPA and accounting firms, and EBITDA is almost always the metric driving their offer. Private equity is a complex marketplace, and we include “roll-up” buyers in that definition. A “roll-up” is a firm that is buying accounting firms usually to play arbitrage with multiples. They buy many smaller firms at a lower multiple and sell to a larger roll-up or PE at a higher multiple.

What is SDE?

SDE stands for Seller’s Discretionary Earnings. SDE is the standard cash flow metric used in “main street” M&A transactions, which is where most CPA firms and accounting practices fall. It is the metric buyers and lenders use for owner-operated businesses with revenues generally under $5 million. There is nothing magical about the $5 million benchmark and there are firms well under $3M that could and should be analyzed using EBITDA instead of SDE.

SDE measures the total financial benefit to a single owner-operator. It includes EBITDA, plus the owner’s salary, plus owner perks (auto, insurance, retirement contributions), plus any one-time non-recurring expenses. The premise is simple: a buyer who is going to step in and run the firm themselves will receive all of these benefits, so they should all count when calculating what the firm is “really” earning.

The Practical Difference

The cleanest way to see the gap is to walk through a real example. Take a CPA firm with the following profile:

A CPA practice with $1,500,000 in gross revenue in Arizona can yield different valuations depending on whether a Seller’s Discretionary Earnings (SDE) multiple or an Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) multiple is applied.

SDE values the business from the perspective of an owner-operator who works in the business, while EBITDA values it from the perspective of an institutional or hands-off investor. Below is a detailed, multi-layered financial example demonstrating how these two methodologies diverge for the exact same firm.

1. Establish the Baseline Financial Assumptions

To compute both metrics accurately, we assume typical profitability and operational structures for a $1.5M accounting firm in Arizona:

- Gross Revenue: $1,500,000

- Operating Expenses (excluding owner compensation): $900,000

- Net Operating Income (Pre-Owner Pay): $600,000

- Owner’s Actual Salary & Perks: $250,000

- Replacement Fair Market Salary for an Employee CPA: $150,000

- Interest, Depreciation, & Amortization: $20,000

2. Calculate the Valuation Metrics (SDE vs. EBITDA)

SDE adds back the owner’s total compensation because it assumes the buyer will replace that owner-operator. EBITDA replaces the owner with a market-rate employee salary because it assumes a corporate or hands-off buyer.

|

Financial Line Item |

SDE Calculation |

EBITDA Calculation |

|

Gross Revenue |

$1,500,000 |

$1,500,000 |

|

Operating Expenses |

-$900,000 |

-$900,000 |

|

Interest, Tax, Depr. & Amort. (EBITDA) |

(Excluded from expenses) |

(Excluded from expenses) |

|

Owner’s Compensation & Perks |

+$250,000 (Added back) |

-$150,000 (Subtracted as Market Salary) |

|

Final Earnings Metric |

$600,000 (SDE) |

$450,000 (EBITDA) |

3. Apply Market Multiples for Arizona CPA or Accounting Firms

Accounting practices are highly sought after for their recurring revenue models. In the local Arizona market, a $1.5M firm generally commands the following benchmark industry multiples:

- SDE Multiple Range: 2.0x to 3.5x (Typically purchased by individual Operators)

- EBITDA Multiple Range: 3.5x to 5.5x (Typically purchased by regional firms or Private Equity)

Using a mid-point market multiple for each category yields the following valuation divergence.

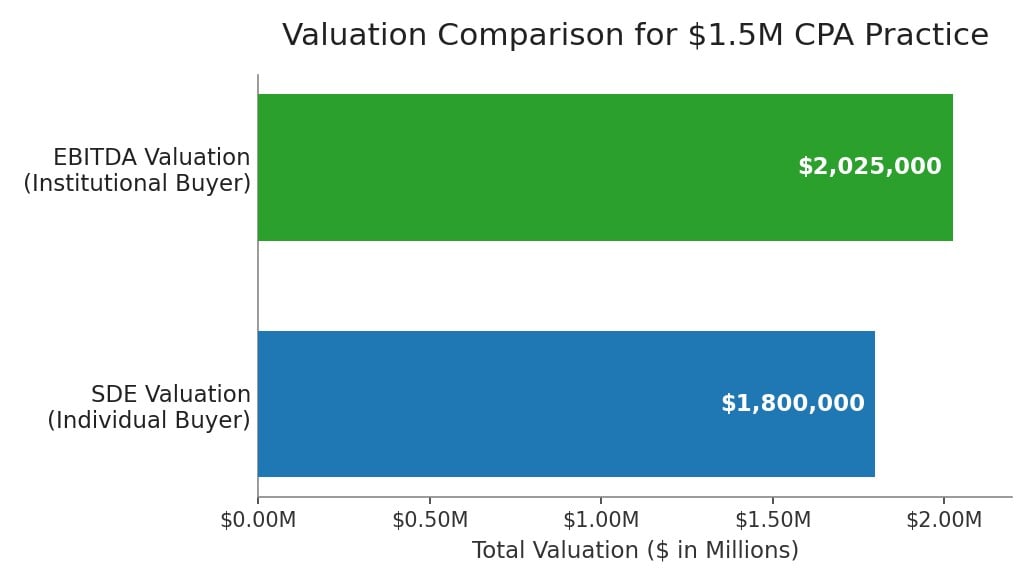

SDE Valuation Path $600,000 SDE x 3.0x Multiple = $1,800,000

EBITDA Valuation Path $450,000 EBITDA x 4.5 Multiple = $2,025,000

4. Analyze the Valuation Gap and Blind Spots

The $225,000 price premium generated by the EBITDA method highlights critical structural nuances that buyers and sellers must navigate:

- The Buyer Profile Dictates the Metric: An individual CPA utilizing an SBA 7(a) loan will generally value the firm on SDE ($1.8M) because they intend to work the book. Regional firms or private equity platforms consolidating the Arizona market will value it on EBITDA ($2.025M) because they will hire a replacement CPA/Accountant to preserve operations.

- Deal Structure Adjustments: While the EBITDA valuation is higher, corporate buyers rarely pay 100% cash at closing. Expect a mix of earn-outs (e.g., 20% to 30% tied to client retention). In addition, many private equity and roll-up buyers make offers with something called rolled equity (at topic for another day). Individual SDE buyers using SBA loans often provide higher upfront cash percentages (typically 80% to 90% financed by the bank). In some cases, buyers are giving 100% cash out to the seller when competitive forces demand it.

- Arizona Regional Factors: Firms located in high-growth Arizona hubs like Phoenix or Scottsdale, generally push toward the top end of both multiple ranges due competition for well-run firms in our lucrative market.

Which Multiple Applies to Each?

This is where it really matters. The multiple a buyer applies to earnings is different depending on which earnings figure is in play.

For SDE-based transactions in the CPA and accounting space, multiples typically run between 2 and 3.5 times SDE for healthy firms with strong margins. You will more often hear value expressed as revenue multiples vs SDE. Earnouts are often tied to revenue and so expressing the price in terms of a revenue multiple makes negotiating the earnout easier. Revenue multiples generally .75 to 1.6 times gross recurring revenue maps closely to the SDE multiple math.

For EBITDA-based transactions, particularly with private equity buyers entering the accounting space, multiples can run higher, often 4 to 12 times EBITDA, sometimes more for very large platform deals.

This is why understanding which metric is being used is critical the moment you start any sale conversation, especially with private equity buyers or their roll-up equivalents, who arrive quoting EBITDA multiples.

When SDE is the Right Metric for Your Firm

For many CPA firms and accounting practices in the under-$3M revenue range, SDE is the right earnings metric. You are an owner-operator. The buyer is most likely another owner-operator. The total economic benefit you currently receive (salary, perks, profit) is what the buyer is realistically stepping into. That being said, there are many firms under the $3M hurdle that can and should receive an EBITDA based valuation.

Some intermediaries use the term “cash flow” which is nebulous. Both EBITDA and SDE are “cash flow” metrics but as you can see, they are very different. EBITDA multiples will always be higher than SDE multiples. The cash flow used for EBITDA will always be lower than an SDE calculation on the same firm.

When EBITDA Comes Into Play

EBITDA becomes more relevant when:

- Your firm has a fully professional management team and you, the owner, no longer fill a production role.

- You are negotiating with a private equity buyer or strategic acquirer who plans to roll your firm into a larger platform.

- Your firm is approaching or exceeding $3M in revenue and starts to enter institutional-buyer territory.

- A buyer plans to install professional management rather than operate the firm personally.

Even in these cases, a strong advisor will calculate both figures so the seller can see the full picture and negotiate from a position of clarity.

The Bottom Line for CPA Firm Owners

If you are exploring a sale of your accounting practice and get an offer, the first question to ask any potential buyer or broker is: “What earnings metric are you using and what multiple are you applying to it?” The answer will tell you immediately whether you are being valued as a main street practice (SDE) or as an institutional asset (EBITDA), and whether the offer in front of you is genuinely strong.

We use both EBITDA and SDE multiple analysis where possible. The size and EBITDA requirements for large buyers are changing all the time due to competitive forces and so it’s very likely that both institutional buyers and owner operators will be competing for the same firm. This bi-furcated valuation model is complicated to negotiate.

For a deeper look at how supply, demand, profitability, and other factors set your firm’s multiple, see our guide on valuing your CPA firm or accounting practice.

Curious what your firm is worth?

Berkshire Business Sales & Acquisitions specializes in valuing, packaging, and selling accounting and CPA practices. Schedule a confidential conversation and we will run both SDE and EBITDA frameworks on your firm so you can see the full picture. We will also discuss the positives and negatives of various buyer types for your particular situation. Having someone on your side that understands these nuances can help you navigate this bi-furcated buyer pool and achieve your long-term goals.

If you’re looking to sell your CPA or Accounting firm in Arizona, contact Ryan by using the form below or calling 602-614-3583.