For many CPA firm and accounting practice owners, one of the most common questions during exit planning is simple:

What is my accounting practice actually worth?

In 2026, the answer is more complex than ever. Valuation multiples for accounting practices are influenced by far more than just revenue or cash flow margins. Market conditions, buyer demand, staffing, revenue mix, revenue growth and the technology the firm deploys all play significant roles (in addition to revenue and cash flow metrics) in determining the price a buyer is willing to pay.

At the same time, the accounting acquisition market is evolving. Private equity firms, regional accounting groups, and individual owner-operators are all competing for acquisitions, and each group evaluates practices differently.

Understanding the mechanics behind valuation — and what truly drives multiples — can help accounting practice owners prepare for a successful exit.

Quick Answer: How Accounting Practices Are Valued Today

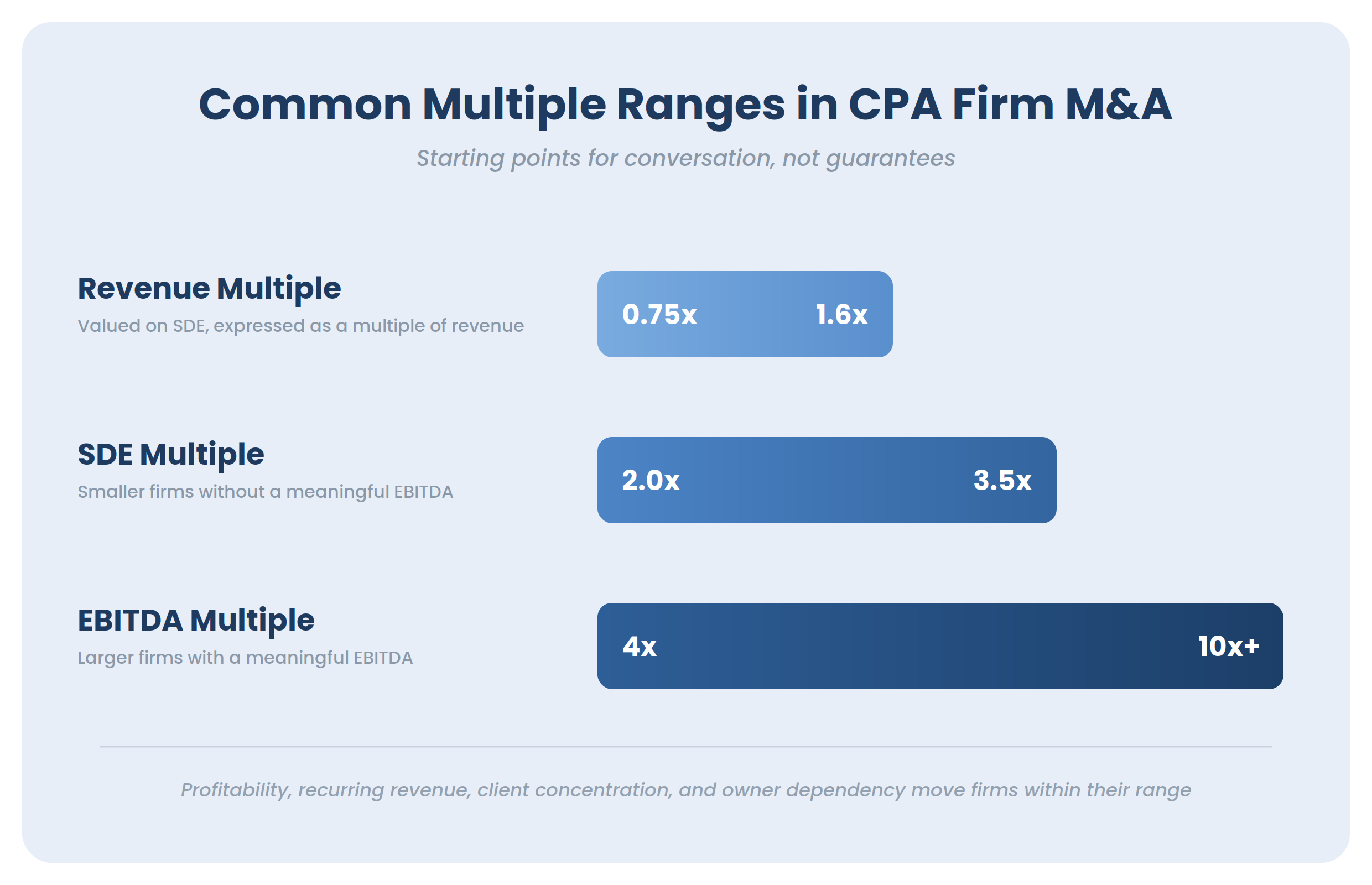

Most accounting practices are valued using a multiple of normalized earnings (EBITDA or SDE). Small firms are valued using SDE but are generally expressed as a multiple of gross recurring revenue. The two most common valuation metrics are:

- SDE (Often “expressed” in terms of a multiple of revenue) for smaller firms

- EBITDA for larger firms with established teams

The final value and multiple depends on factors such as:

- Cash flow margin (SDE or EBITDA)

- Quality of Earnings

- Client concentration

- Staffing complement

- Owner dependency

- Revenue mix

- Technology deployment

- Demand and supply

In other words, the multiple is simply the market’s way of pricing future predictability and risk.

Revenue vs EBITDA Multiples Explained

One of the biggest sources of confusion in accounting practice valuation is the difference between Revenue and EBITDA multiples.

Gross Recurring Revenue

For firms less than one million dollars in top-line revenue, it is difficult to come up with a meaningful EBITDA number. It’s for this reason that most small firms’ valuation is expressed as a multiple of gross recurring revenue. While these are expressed as a revenue multiple, these small firms are actually valued using SDE (seller discretionary earnings) and the SDE margin. The SDE multiple range is typically 2-3.5x. Small firms with very high SDE margins are priced higher in the multiple range. Firms with skinny SDE margins are priced lower on the multiple scale. Small firms have historically sold between .75 and 1.6 of gross recurring revenue which roughly equates to SDE multiples of 2-3.5x.

Seller Discretionary Earnings represents the total financial benefit available to an owner and typically includes:

- EBITDA

- Plus, one owners W2 wages and burden

- Plus, certain discretionary expenses and other benefits that flow to the owner

- Plus, or minus non-recurring adjustments

Because many small accounting firm owners structure compensation differently, SDE provides a clearer picture of the true cash flow available to a buyer. In essence, SDE is the cash flow before the buyer takes a salary and before debt service. Banks will qualify these deals using an SDE calculation.

EBITDA

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. This metric is used more frequently for larger accounting firms with multiple partners, managers, and operational infrastructure (typically greater than 1M).

Buyers using EBITDA typically include:

- Regional & National accounting and CPA firms

- Private equity-backed platforms & roll-up buyers (aggregators)

- Strategic Buyers

These buyers evaluate the firm as an enterprise rather than simply replacing the owner’s income.

Why Multiples Are Changing in the Accounting Industry

One of the most important changes affecting accounting practice valuation is the shift in the buyer landscape.

Historically, most accounting practices were sold to owner-operator buyers — usually another CPA looking to grow their firm.

Today, however, private equity and aggregator groups are increasingly active in the market, which has changed how deals are structured and priced.

Private equity is attracted to accounting firms for several reasons:

- Highly recurring revenue

- Fragmented industry structure

- Opportunities for consolidation

- Cross-sell opportunities

- Potential operational efficiencies through technology and outsourcing

These firms often pursue roll-up strategies, acquiring multiple smaller practices and combining them into larger organizations.

The Two Buyer Types Affecting Valuation

Today’s accounting practice owners often face a decision between two primary buyer categories.

Owner-Operator Buyers

Owner-operators are usually credentialed CPAs who plan to personally operate the firm.

These buyers typically:

- Have strong technical expertise

- Focus on client relationships

- Offer more conservative valuations

- Prioritize cultural alignment and continuity

Many small practice sellers prefer this type of buyer because the firm often continues operating in a similar structure.

Private Equity and Strategic Buyers

Private equity groups and aggregators approach acquisitions differently.

Their strategy often involves:

- Acquiring multiple practices

- Standardizing operations

- Increasing margins

- Eventually selling the larger platform firm

Because of this model, they sometimes pay higher prices for acquisitions in competitive situations. However, the structure and long-term direction of the firm may change significantly after the transaction.

Supply and Demand in the CPA Firm Market

Another factor influencing valuation multiples is the changing supply and demand dynamics in the accounting profession.

Several trends are shaping the market:

- A large number of baby boomer CPA firm owners are reaching retirement age

- Fewer younger CPAs are interested in purchasing practices

- Consolidation activity is increasing across the industry with private equity demand

This combination means the buyer pool is evolving, which directly impacts valuation outcomes for many firms. In some cases, increased competition among buyers can push multiples higher. In others, a limited number of qualified owner-operators may reduce demand for certain practices.

Retention Risk: The Biggest Driver of Deal Structure

One of the most critical factors in accounting practice transactions is client retention.

Most acquisition agreements include retention clauses, meaning the final purchase price depends on how many clients stay after the transition. That is also why confidentiality during an accounting firm sale matters so much, since premature conversations with clients, employees, or competitors can create uncertainty before a transition plan is in place.

Industry surveys often estimate 75–80% retention following a sale, although strong transitions can exceed that average.

Retention risk increases when:

- The owner handles most client relationships personally

- The mix of clients is mostly 1040

- Other staff leave when the principal leaves

- Locations, pricing or operations are significantly changed

- Clients are concentrated in a few large accounts

Some buyers factor this risk directly into the valuation multiple. Others structure the deal so that this risk is mitigated.

Client Concentration and Revenue Stability

Another major valuation driver is client concentration.

A firm where a handful of clients generate a large percentage of revenue is considered higher risk.

For example:

- A firm with 1500 recurring clients and no concentration often commands stronger multiples.

- A firm where three clients represent 40% of revenue may receive lower offers or may receive a much different offer structure with less cash up front and more based on retention numbers after sale.

Diversification creates more predictable revenue, which buyers value highly.

Transition planning can increase the amount you receive for your practice

Many accounting firm owners underestimate how much transition planning affects retention. Buyers want to see a clear path for transferring relationships and operations after the sale.

Strong transition plans typically include:

- Seller involvement for a defined period

- Joint client introductions

- Clear communication with employees & clients

- Documentation of workflows and systems

Without a structured transition, buyers may assume a higher risk of client loss.

Why Inflated Multiples Often Lead to Failed Deals

Some national marketplaces promote optimistic valuation multiples to attract sellers.

However, these numbers often represent idealized scenarios that assume:

- High client retention

- Strong staff structure

- Diversified revenue

- Minimal owner dependency

When buyers perform due diligence, any weakness in these areas can quickly reduce the valuation.

A realistic valuation grounded in market conditions and firm fundamentals typically leads to smoother negotiations and successful closings.

Arizona Market Considerations

Local market dynamics can also affect valuation outcomes.

In Arizona, several factors influence CPA firm sales:

- Continued population growth driving demand for accounting services

- Private equity is interested in growing metropolitan areas

- Phoenix is on most national or private equity top 10 list for acquisition

These dynamics create opportunities for sellers, but the final valuation still depends heavily on the structure and health of the individual practice.

Preparing Your Firm for a Stronger Valuation

Owners who begin exit planning early often achieve stronger sale outcomes.

Steps that improve valuation include:

- Growing the cash flow margin (EBITDA & SDE)

- Developing a strong entity mix within your practice vs all 1040

- Increase revenue each year

- Developing staff leadership, staff and potential offshoring

- Deploy technology and consider virtual, paperless operations

These improvements make the firm less risky and more attractive to buyers. Learn more on how to sell your accounting practice.

The Bottom Line

Accounting practice valuation is ultimately about predictability.

Buyers pay higher multiples when they believe the firm’s revenue, clients, and operations will remain stable after the owner exits.

Understanding these drivers allows firm owners to make strategic improvements well before bringing the practice to market.

Considering the Sale of Your Accounting Practice?

If you are thinking about selling your CPA or accounting firm, an accurate valuation is the first step toward a successful exit.

Berkshire Business Sales & Acquisitions specializes in broker-led transactions for accounting and CPA practices, helping owners:

- Understand realistic market valuation multiples

- Prepare their firms for sale

- Identify qualified buyers

- Structure transitions that protect client relationships

With the accounting M&A landscape continuing to evolve, working with a brokerage that focuses specifically on CPA practice transactions can make a significant difference in both price and deal quality.

Ready for a Clearer Picture of Your Firm’s Value?

Talk with Berkshire about what your accounting practice may be worth and what steps could help you prepare for a stronger exit.